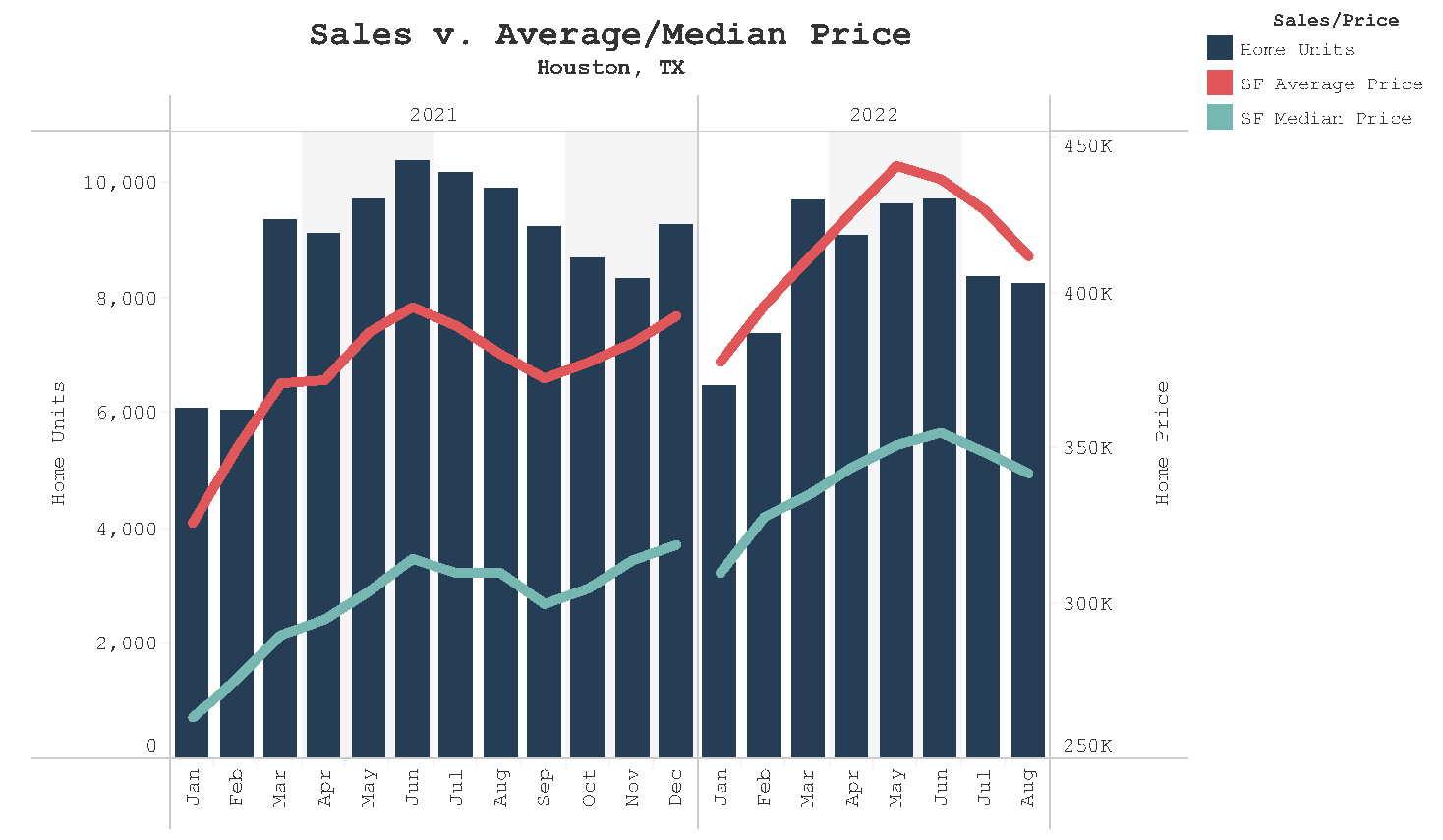

Home Sales Flatten, but Price Drops Accelerate

Home sales slowed in August from the free fall in July likely due to a combination of factors, including a quick drop in mortgage rates and price cuts. Because of seasonality, home sales in August typically begin to level out or fall off after the summer rush to buy homes due to the school summer break. While home sales could have fallen off from July in more dramatic fashion, it seems sales have been supported by a quick jolt of lower of interest rates in August, which dipped slightly below 5% at one point. August sales numbers also likely remained flat because home sellers have started to make concessions with home prices dropping over 3% from July. The Average and Median home prices in Houston sit at $411,671 and $341,950, respectively, representing a 3.5% and 1.9% drop from July.

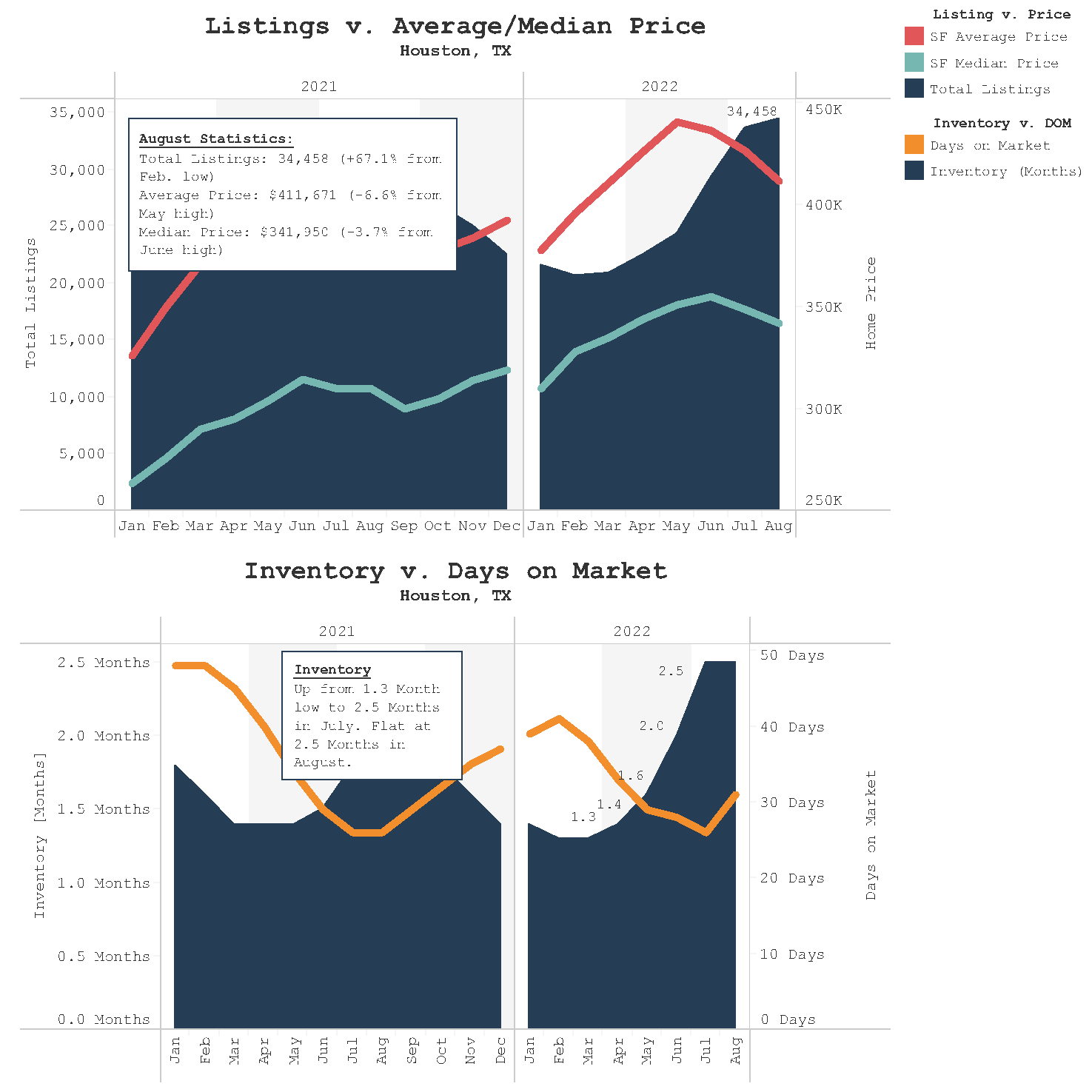

Inventory Increases Slow as Seasonality Kicks In

As you would also expect, seasonality trends don’t only affect home sales. They also affect the inventory trends. Inventory began to level out at 2.5 months (or 34,458 listings), a slight increase over July. This slowdown is not unusual because listings typically rise in the summer months and begin to slow afterwards.

While we are a long way off from the typical “neutral” market indicator of 6 months’ inventory, we are steadily headed in that direction. Every month since February has notched significant increases as sellers have tried to sell while interest rates remained moderate. Total inventory has nearly doubled in the months from February to July and will likely continue to rise as buyer sentiment fades in the face of the quickest rate increases in 40 years.

Mortgage Rates Drop in August, but Rise in September

Mortgage rates dropped slightly in August, giving buyers an opportunity to lock rates in for another 60 days. This will likely be a quick injection of demand for the next month or two. However, rates quickly stormed back higher in September so we can expect this to continue to pressure sales and prices going forward. As of this writing, the average rate on a 30-year mortgage currently sits at 6.29% interest, a level not seen the 2008 financial crisis. As an even more bleak outlook, rates are expected to continue to go higher in the coming years to combat the sustained inflation which has taken place per the federal reserve.

*The graph above only depicts rates through start of August. This is due to the match the rest of the data, which is collected on a trailing basis. It does not reflect the current rate environment, which showed an increase to above levels of 6% in September as of this writing.

Rents Continue to Rise

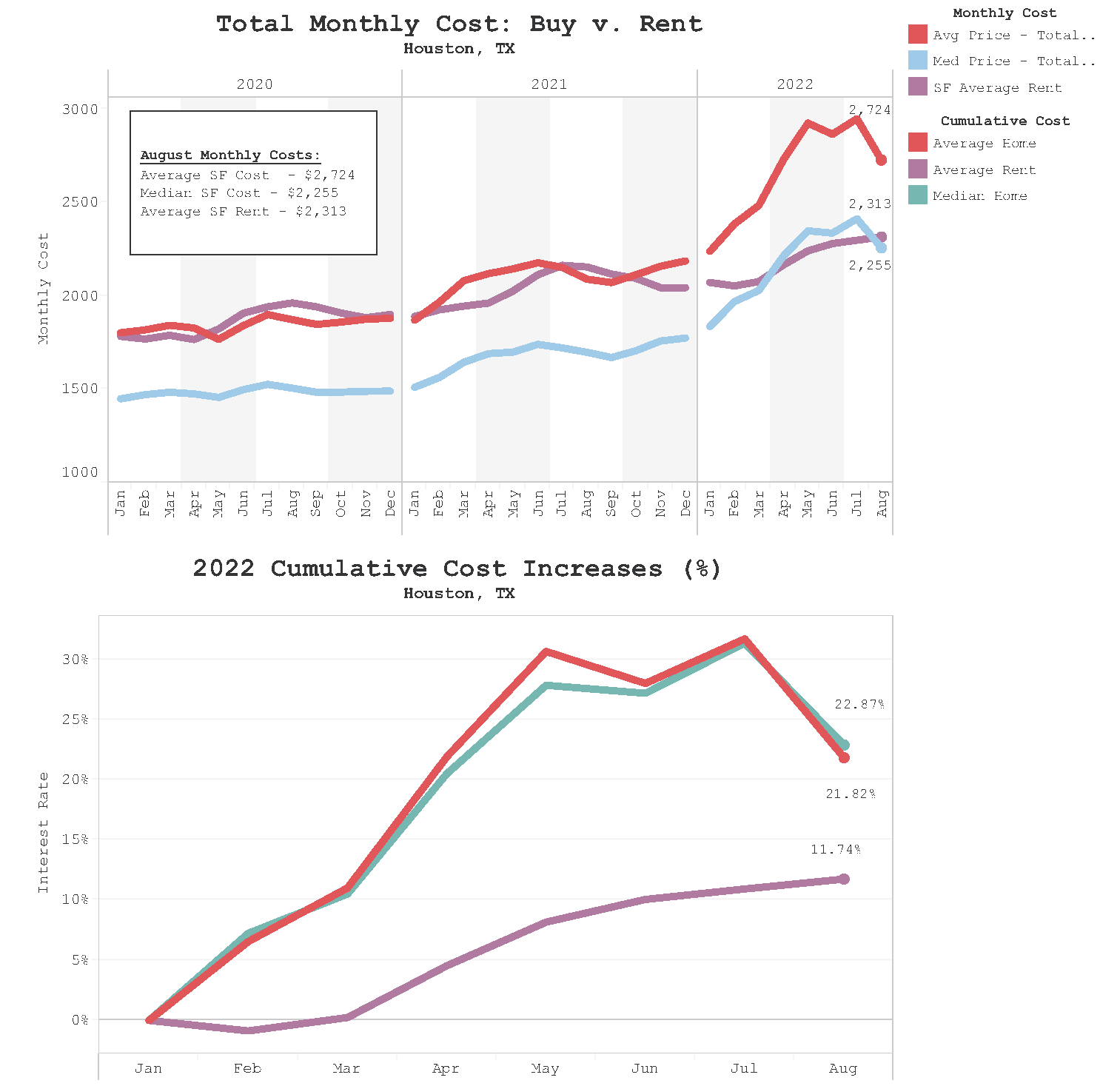

Unfortunately for many new buyers, your only alternative (besides living with family) will be renting in a market where increasing rental rates seem to be the theme and not the outlier. Rental rates on Single Family properties from $2,296 to $2,313, a 0.7% increase. However, rents for townhouses showed some signs of easing with the average rent moving from $1,925 in July to $1,924 in August.

Until housing prices drop significantly into more affordable territory (as depicted in our rent v. buy comparison), the best alternative to buyers will be to rent. This imbalance of demand for rental properties may continue to cause upward pressure in rents until home prices correct in the face of higher inventories and higher interest rates over the course of the next 12 months.

Comparing Value: Rent v. Buy Chart (September 2022)

Future Expectations for 2022

With a sustained and predictable rise in the federal funds rate and interest rates throughout the year, downward pressure on the Housing market should continue to occur. The housing sector (and real estate writ large) is one of the most sensitive industries to monetary policy and interest rates. The cause and effects of such rate increases are known, and you can expect home prices to continue their drop over the next 6 – 9 months, potentially longer.

Inventories will likely increase over the next 6-12 months, but at a slower rate than you’d expect. Many of today’s homeowners were able to lock in fantastic interest rates (sub 4% and below) in 2021 and early 2022. Because of this, many homeowners aren’t willing to sell their properties to buy new ones because of they would have to swap out the great rate they’ve received for a poor rate.

As for rents, expect them to slowly creep up or flatten out. While the effects of the Federal Reserve’s hawkish stance remain to be seen, the increase in demand for rental properties due to a lack of alternatives should keep rents and rental rates moving in an upward or flat trajectory. Expect it to be sticky for a while.

© 2022 Parceto LLC, d.b.a. Parceto Real Estate, all rights reserved.

Online Information Sources:

Third-party image sources: shutterstock.com, adobe.com

Freddie Mac, “Mortgage Rates.” Freddiemac.com, 21 Sep 2022, https://www.freddiemac.com/pmms

Houston Association of Realtors, “Houston Housing Remains Robust in August as the Market Cooldown Continues”

Har.com, 14 Sep 2022, https://www.har.com/content/department/mls?y=2022&m=09

Houston Association of Realtors, “Single-Family Rental Homes Draw Strong Consumer Demand in August” Har.com,

21 Sep 2022, https://www.har.com/content/department/newsroom?pid=1878